Vega and Earnings: Playing Volatility the Right Way

Vega and Earnings: Playing Volatility the Right Way

Earnings season is the Super Bowl of options trading. Every quarter, hundreds of companies report results that can send stocks soaring or cratering in after-hours trading. And around every one of those announcements, something predictable happens to options prices — something that experienced traders have been exploiting for decades.

It’s called the volatility cycle. Understanding it is the key to trading earnings intelligently rather than randomly.

What Is Vega?

Vega (ν) measures how much an option’s price changes for every 1-percentage-point move in implied volatility (IV).

An option with a vega of $0.20 gains $0.20 in value for every 1% rise in IV, and loses $0.20 for every 1% fall.

Where theta is driven by time, vega is driven by uncertainty. When the market perceives more uncertainty about a stock’s future — say, right before an earnings announcement — implied volatility rises, and options prices swell. When the uncertainty resolves (the number comes out), implied volatility collapses, and options prices deflate.

This deflation has a name: IV crush.

IV Crush: The Event That Defines Earnings Trading

Here’s the earnings IV cycle in action:

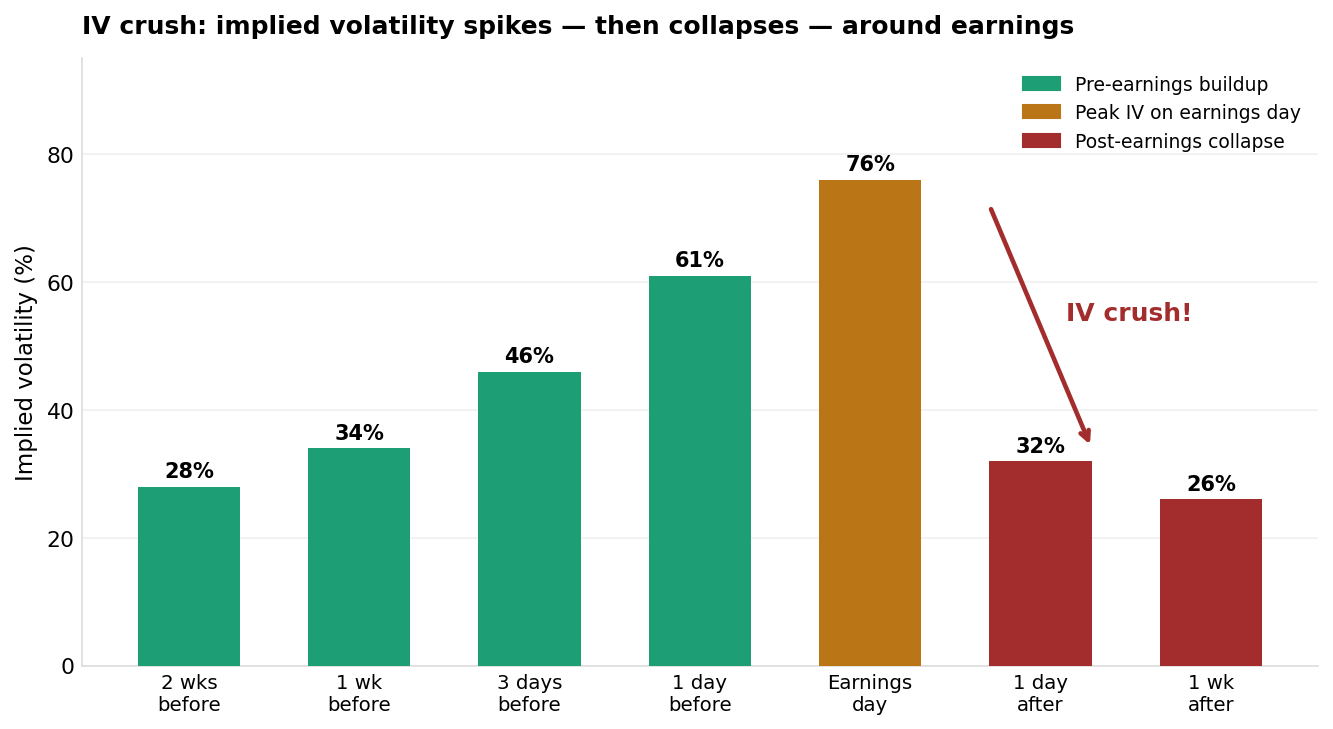

Implied volatility builds steadily in the weeks before earnings, peaks on announcement day, then collapses sharply the day after — even if the stock makes a big move.

Implied volatility builds steadily in the weeks before earnings, peaks on announcement day, then collapses sharply the day after — even if the stock makes a big move.

The pattern is remarkably consistent across most stocks:

Weeks before earnings: IV slowly rises as traders buy options to position for the announcement. Demand drives premiums higher.

Day before earnings: IV is at peak — often double or triple the stock’s “normal” volatility. Options prices are at their richest.

Earnings day (after the announcement): IV collapses immediately, often by 40–60% in a single session. This happens regardless of whether the stock moves up, down, or sideways.

The week after: IV returns to its baseline, near where it was before earnings season began.

Why IV Crush Is Dangerous for Buyers

Suppose you buy an AAPL call option before earnings, expecting a big move. The stock rises 5% after the announcement — your directional bet was correct. But you might still lose money on the trade.

How? Because the option was priced for 76% implied volatility before earnings and repriced for 32% implied volatility after. The 5% stock move was not enough to offset the collapse in time value. Your option lost more from IV crush than it gained from the stock move.

This is the trap that catches most options buyers around earnings: being right about direction but wrong about the magnitude.

How Traders Play Earnings with Options

There are two legitimate approaches, each suited to different risk tolerances:

Approach 1: Sell the Vol (Short Volatility)

If IV reliably spikes before earnings and reliably collapses after, why not be the person selling the expensive options?

A short strangle or short straddle placed before earnings involves selling both a call and a put on the same stock. You collect premium when IV is elevated. When IV collapses after the announcement, both options lose value — you buy them back cheaply and keep the difference.

The risk: If the stock makes an extremely large move in either direction — bigger than what the options market “implied” — you can lose significantly. This is not a risk-free strategy. Position sizing is critical.

The historical edge: Some academic and practitioner research has found that options markets have historically tended to overprice expected moves around earnings — meaning the actual stock move came in smaller than the implied move often enough to give systematic sellers a statistical advantage. However, this edge is not guaranteed. It has been contested in the literature, has compressed as more traders have moved into earnings volatility strategies, and individual events still carry significant tail risk. Treat this as a historically observed base rate to inform your decision, not a reliable income stream.

Example setup — AAPL earnings:

Stock at $170, earnings tomorrow

Sell 1x $165 put expiring 1 day after earnings — receive $3.20

Sell 1x $175 call expiring 1 day after earnings — receive $3.00

Total premium: $6.20 per share ($620 per strangle)

Profit if AAPL stays between $158.80 and $181.20 at expirationApproach 2: Buy the Vol (Long Volatility)

If you have a strong conviction that the stock will make a very large move — larger than what the market is pricing in — you can buy volatility before the announcement.

A long straddle (buy call + buy put at the same strike) profits if the stock moves significantly in either direction. You don’t need to be right about direction, only about magnitude.

The risk: IV crush will hammer your position the morning after earnings. Even if the stock moves as expected, you need the move to exceed your total premium paid to turn a profit.

This trade is harder to execute profitably than most beginners expect, because the market is generally efficient at pricing earnings uncertainty. The options market has seen thousands of earnings cycles.

A Key Concept: Implied Move

Before every earnings announcement, the options market “implies” an expected move — a range within which the stock is statistically likely to settle. Traders calculate this from the at-the-money straddle price.

Implied move formula: Straddle price ÷ Stock price = Implied move %

If the $170 ATM straddle is priced at $8.50 total, the implied move is approximately $8.50 / $170 = 5% in either direction.

This is your benchmark. If you think AAPL will move more than 5%, buy the straddle. If you think it will move less than 5%, sell the strangle. If you have no strong view on the magnitude, stay on the sidelines.

Vega Risk in Non-Earnings Positions

IV crush isn’t just an earnings phenomenon. Any event that resolves uncertainty — Fed meetings, drug trial results, regulatory decisions — can cause localized IV spikes and collapses.

For income sellers running ongoing covered calls or cash-secured puts, be aware that positions held through earnings events carry vega risk. If you sell a put the week before earnings on a high-IV day and the company beats estimates, you might get a double benefit (stock rises + IV collapses). But if the stock misses badly, you’re facing both directional loss and continued elevated volatility.

General rule for income sellers: avoid holding short options positions into earnings on individual stocks unless you are intentionally running a volatility strategy and sizing appropriately.

Key Takeaways

- Vega measures an option’s sensitivity to changes in implied volatility; options with high vega gain value when IV rises and lose value when IV falls

- IV crush occurs when implied volatility collapses after an earnings announcement — even a big stock move may not offset the premium loss for buyers

- Selling volatility before earnings (short straddle/strangle) is based on the historically observed tendency for implied moves to exceed actual moves — but this edge is contested, has compressed over time, and carries significant risk if the stock makes an extreme move

- Buying volatility (long straddle) profits from larger-than-implied moves but is expensive and often crushed by IV collapse

- The implied move calculation (straddle price ÷ stock price) gives you a benchmark for whether to be long or short volatility

What’s Next

You’ve got the foundational Greeks down. Time to put them to work in your first real income strategy: The Covered Call: Generate Income from Stocks You Own — a complete setup guide with real numbers and a P&L diagram.

For trading around earnings and monitoring IV rank in real time, Tastytrade surfaces implied volatility data prominently across their platform — making it easier to spot when IV is elevated before an announcement and size your position accordingly.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Always conduct your own research and consult a licensed financial advisor before making investment decisions.